-

15

May

LTL Carrier First Quarter 2023 Earnings – Wrap up

As a follow up to the individual carrier recaps I have provided on LinkedIn, I thought I would wrap things up with an overall recap. The 9 publicly-traded LTL carriers I profiled make up about 2/3 of the LTL industry based upon revenue, thus I feel they are an excellent bellweather for where the industry stands today and where it is headed. Here are the overall nuggets gleaned:

- LTL carriers are more focused on generating profits than ever before. Sure, profits matter. They always have. But LTL carriers have better tools in hand than ever to compute and allocate costs properly, and well-prepared to make account-driven decisions.

- Virtually every carrier is clearly articulating an intent to continue improving their OR by 100 to 200 basis points per year. So if an 84 in 2023, an 82 in 2024, and an 80 in 2025. And the carriers are clearly articulating an intent to more than cover inflationary costs we all see every day.

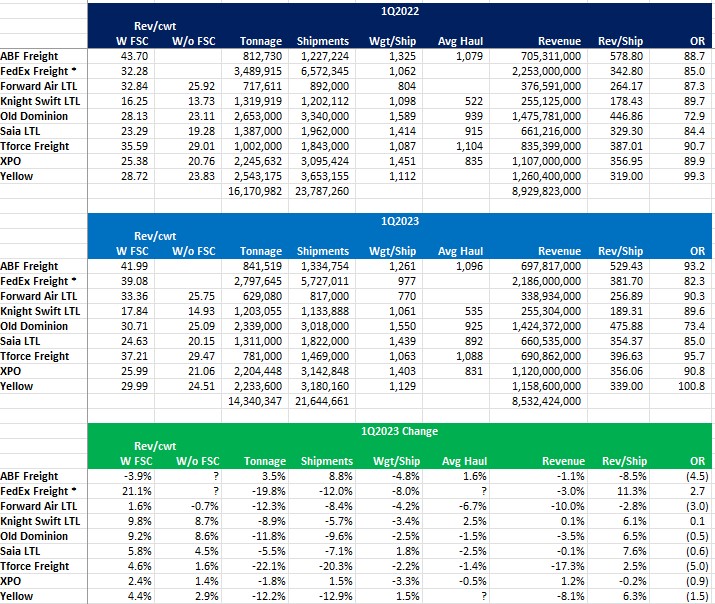

- LTL carriers have immense pricing power, even in todays down freight market. Revenue Per Hundredweight, a good yet imperfect barometer on price, was up around 6% on average when including fuel. Most carriers reported strong contract renewals in the mid to high single digits range.

- Business is definitely down. Tonnage was down 11%, and shipments were down 9%. But revenue was down only 4.5%, as carriers are getting price increases in this market.

- Not only is virtually every carrier super-focused on profits, but they are also super-focused on improving operational and customer service levels, and using that superior performance as a means to charging a premium on prices.

- Even in a down freight market, several carriers are still expanding and looking to strengthen their geographic footprint as they prepare for better times.

- Some of the newer US LTL entrants (Knight-Swift, TFI Intl) tend to report OR by subtracting fuel surcharge revenue from both the cost line and the revenue line. This tends to allow them to report a better OR. Not sure if this is a correct way to compute an OR, so we will see if other carriers use this method.

All in all, the publicly-traded carriers had quite strong results given the softness in business. They managed costs well, and posted pricing gains that allowed them to report relatively strong margins. Full Truckload carriers did not fare near as well. This should set these carriers up quite well when the freight economy improves, and it will.

Interestingly, it seems as if every carrier is actively promoting their plans to be considered the best carrier in terms of performance, and thus having the ability to charge a premium for their services. It remains to be seen if all of these carriers will ultimately be successful. But what intrigues me the most is this question:

Is premium service now table stakes for LTL carriers? Or with everyone chasing the same premium-service philosophy, is a door opening for a carrier to find significant success marketing themselves as economy service at an economy price?

The table below provides 1Q23 vs 1Q22 key metrics. Visit the blog page on my website to download this table in Excel, and find all of the carrier recaps.

- (479) 461-1672

- Contact Us